How to Plan Startup Financing Around Runway and Milestones

Model founder cash, investor rounds, coverage, and buffer around the forecast you already built — so the financing plan reflects the milestones your startup actually needs to reach.

Plan financing timing and see how it changes runway

Add founder funding and investor rounds, then compare the cash path with and without financing over 24 months.

24 months · ending cash with the same monthly burn

Financing is a runway design problem

A round is never only a number on a slide. It is time purchased for a specific stretch of work: hiring, shipping, proving retention, or opening a commercial chapter. A financing plan earns its keep when it makes that chain visible — where modeled cash gets uncomfortable, what milestone sits ahead, and how many months the business needs protected on the path you actually believe in.

Starting from a target raise is a natural shorthand when you are comparing notes with peers or mapping calendar pressure. The model becomes more powerful when you treat that target as an output of runway design rather than the first input. One team might need a single bridge to MVP or first paid logos; another might run founder cash and services income for quarters before an investor event lands. A bootstrapped SaaS product that is already close to break-even may only need financing to avoid slowing down before profit arrives. A deep-tech or biotech company can need a much larger round because the milestone itself is expensive: research, validation, regulatory work, or hardware iteration before meaningful revenue appears. A consumer product with strong early pull might need capital less for R&D and more for team, growth, and working cash while demand catches up to operations.

The shape changes from company to company, but the design logic stays the same. How much time does this next phase need, what has to be true by the end of it, and how much protection is sensible for a team with this product, market, and burn profile. Once those pieces are explicit, the round size stops being an abstract ambition and starts reading like part of the operating plan.

What a round is supposed to buy

A financing event is time purchased for a milestone — with room before the next decision point.

Current path

Modeled cash

Month-by-month burn and inflows from the operating forecast.

Capital in

Financing event

Founder funding or investor cash lands in a specific month.

Coverage window

Runway to work

How long this capital carries the company on the path you modeled.

End of window

Milestone

The proof point this stretch of runway is meant to fund.

Cushion & next step

Buffer, contingency, then the next decision point

Extra months and a margin for slippage sit ahead of the next financing conversation or operating choice.

The headline round size only matters once this chain is coherent.

Cash timing and the forecast underneath

Cash leaves through payroll, acquisition, COGS, overhead, and one-time items. Revenue arrives through pricing, billing cadence, and growth. Financing answers a narrower question on top of that path: when inflows need to land so the business can keep executing until the next proof point.

Everything in that sentence depends on the forecast you already built or are still tightening. Pricing and billing timing, acquisition, cost of revenue, payroll, overhead, and one-time costs shape operating cash long before any round is applied. If those layers are thin or rosy, the financing layer can look tidy while describing a company that does not exist yet. That is why serious raise planning usually sits late in the modeling sequence: the Financing view is a lens on the business model, not a substitute for it.

A familiar pattern is a plan where the round amount feels plausible, but the cash-in month is still optimistic. The business shows a funding gap even though the headline raise would pass a cocktail-conversation test. The model is doing its job when it surfaces that kind of timing risk early.

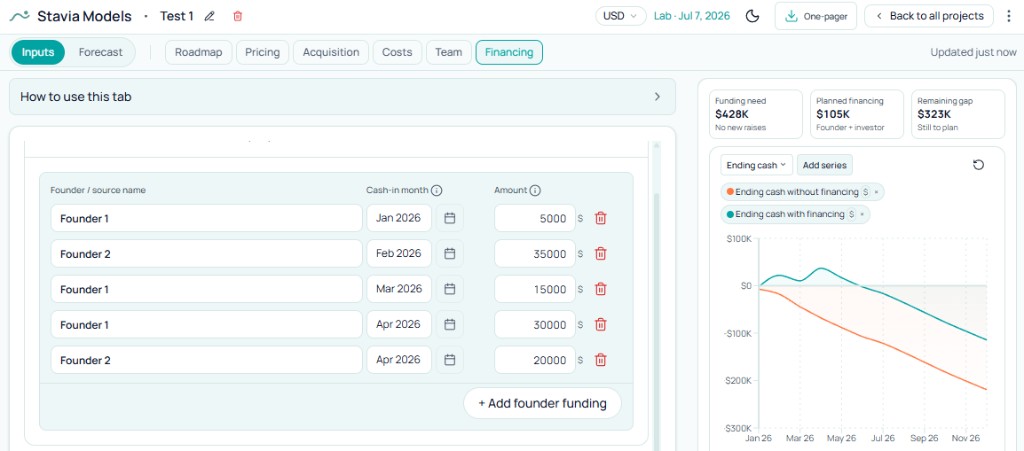

Founder funding counts more than many founders admit

Early capital often arrives before a priced round: personal savings, consulting or services income routed into the company, money from another business, or repeated smaller payments for tools, freelancers, prototype work, and experiments. Those flows rarely feel like "real financing" in conversation, yet the company already consumed them. They changed the cash trajectory the same way an investor wire would.

When those inflows stay out of the model, outside capital looks larger than it really needs to be, and the story of how much runway was already self-funded disappears. Naming each source, the month cash landed, and the amount keeps the financing narrative aligned with how the company actually lived through its first chapters — including the stretch where a services business quietly paid for nights-and-weekends product work before any institutional check.

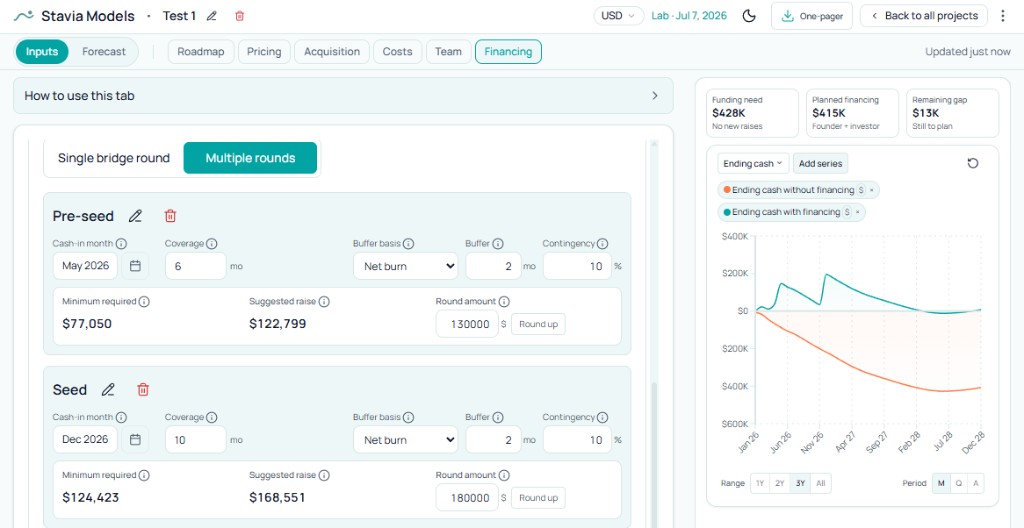

One bridge or several financing events?

One bridge structure fits when the company is effectively funding one continuous milestone path — for example, enough runway to ship an MVP and reach early traction with a single capital injection. The planning question is compact: what one inflow closes the gap between here and that proof point, with room for ordinary delay.

Several financing events fit when the journey naturally breaks into distinct stages: founder cash first, then a small pre-seed to get to launch metrics, then a larger seed for a commercial push. The stages might involve different investors, the same backer in tranches, or a mix of founder and external capital at different dates. What matters is whether you are funding one coherent arc or several chapters that deserve their own timing, coverage, and risk conversation.

If milestones, team shape, and risk profile change materially between chapters, a staged plan usually tells a clearer story than one oversized hypothetical round dated far in the future.

The raise that barely works vs the raise you can live on

In any serious model there are two different ideas hiding inside one round line. The first is the tight floor: the smallest amount that keeps modeled cash from dipping below zero in the window you care about. The second is a more livable raise: that floor plus contingency and buffer so hiring slips, revenue lags, or a milestone takes longer without instantly forcing another financing conversation.

The gap between those two figures is where fundraising stops being a spreadsheet exercise and becomes a judgment about how much uncertainty the company should survive. Mathematically enough is often operationally thin: it assumes the next twelve to eighteen months will behave like the cells you typed. The more survivable number leaves air in the plan for the quarter that does not.

Convenience rounding after you have chosen a direction is fine; it should not replace the decision about how much room you want before the next decision point.

Coverage, buffer, and contingency

Coverage is how long a financing event is meant to carry the company on the modeled path. Buffer adds deliberate extra months on top of that path. Contingency adds margin for things taking longer or costing more than expected. Together they translate a founder's risk appetite into something the forecast can stress-test.

A short window to finish a scoped build can run with less cushion than a multi-quarter commercial ramp where payroll and acquisition move in parallel. The settings only matter insofar as they reflect how brittle the next stretch of the business really is.

How to see the funding gap before it becomes a crisis

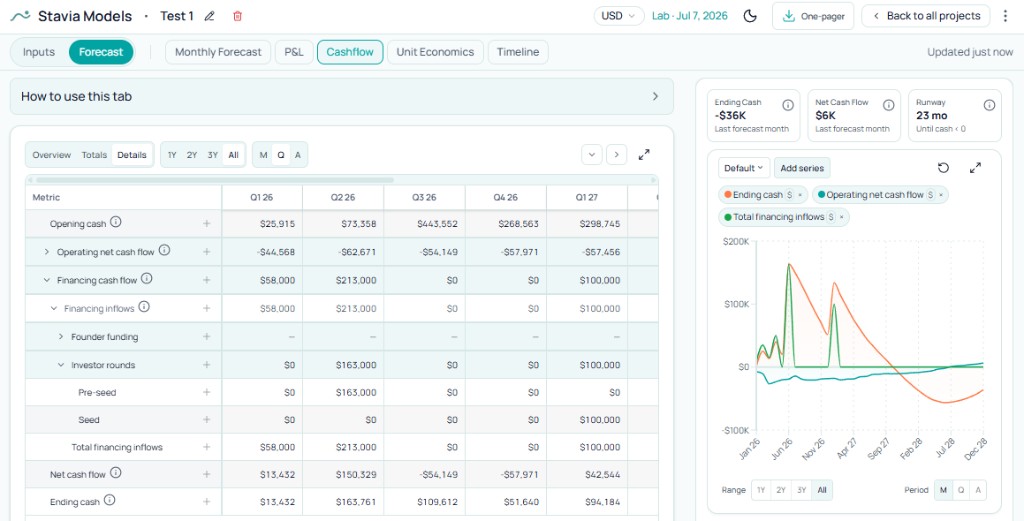

Funding need, planned financing, and remaining gap exist to answer a blunt question: does the capital you have actually entered close the operating shortfall the model sees? A remaining gap means something is still misaligned — round sizes, empty rows, late cash-in months, or a heavier operating forecast than the financing story assumed.

In the cashflow view, financing inflows appear as real quarters alongside operating burn. If ending cash with financing still drifts toward trouble, the plan is better than no plan, yet it is still underbuilt. Treat the gap as a planning signal: the model is pointing at a mismatch between story and cash path.

Why financing is only as good as the forecast underneath it

Funding need and raise suggestions inherit the operating cash and earnings path you built. They do not float in a separate universe. That is worth repeating after you have worked inside the financing view for a while: the credibility of the runway story rises and falls with pricing, acquisition, COGS, payroll, overhead, and one-time assumptions.

If you want the financing chapter to feel grounded, the supporting work is spread across the rest of the model — pricing and billing, paid acquisition, cost structure, cost of revenue, overhead timing, and payroll timing. Read the cash path through a startup cash flow and runway model before the raise size feels real. Once the round size is set, startup use of funds planning connects allocation, sequencing, and milestone evidence to the same operating forecast.

How it works in Stavia

- Build the operating forecast first. Pricing, acquisition, COGS, payroll, overhead, and one-time costs create the cash path that financing has to support.

- Add founder funding as real inflows by source, month, and amount so self-funded runway is visible in the same plan as outside capital.

- Decide whether the company is best described by one bridge or by several financing events across distinct milestones.

- Set the timing and structure of each event: cash-in month, coverage, buffer, contingency, and round amount where that mode applies.

- Read funding need, planned financing, remaining gap, and ending cash with and without financing together. That is where the financing plan becomes a staged runway view instead of a single headline figure.

Common mistakes

Conclusion

The strongest financing plans read like runway design: honest operating assumptions, founder inflows where they really landed, capital events timed against the cash curve, enough coverage to reach the next milestone, and enough cushion to absorb normal variance.

A model earns its place in fundraising prep when it shows why money is needed, when it should arrive, and what proof point that window is supposed to buy. That clarity is what keeps the conversation anchored in the company you are building. The financing layer sits on top of a startup runway and fundraising model that connects operating assumptions to capital timing.

About the author

Anastasiia Nikolaeva

Founder of Stavia Models

Anastasiia Nikolaeva is a financial modeling consultant and the founder of Stavia Models. She has built financial models for SaaS, AI, marketplace, and other startup business models, helping founders plan pricing, growth, fundraising, and unit economics. Stavia Models is based on this hands-on consulting experience and turns that modeling logic into a guided product.