How to Read Startup Cash Flow and Runway Before It Becomes a Problem

Cash flow is where startup timing becomes visible. This view helps founders see when money actually comes in, when it goes out, how financing changes the path, and how much runway the business really has.

Why cash flow needs its own view

A startup can move revenue, gross margin, or EBITDA in the right direction and still face a dangerous cash month. That happens because operations are a timeline: payroll lands on set dates, acquisition spend often leads collections, annual agreements concentrate cash in specific renewal windows, one-time legal or launch work hits a single period, and financing arrives in lumps. None of those forces distribute themselves evenly across the calendar.

Cash Flow deserves its own view because it answers whether the company can survive the timing of its own strategy month by month. When you read Cash Flow as a forward-looking planning lens, surface averages stop substituting for the path.

Cash Flow is a forward-looking planning lens, not only historical accounting output. P&L explains operating structure. Unit economics explains customer-level quality. The detailed step-by-step forecast explains mechanics. Cash Flow answers the survival question in sequence: can this plan be funded through each month as modeled?

What the cash flow forecast shows

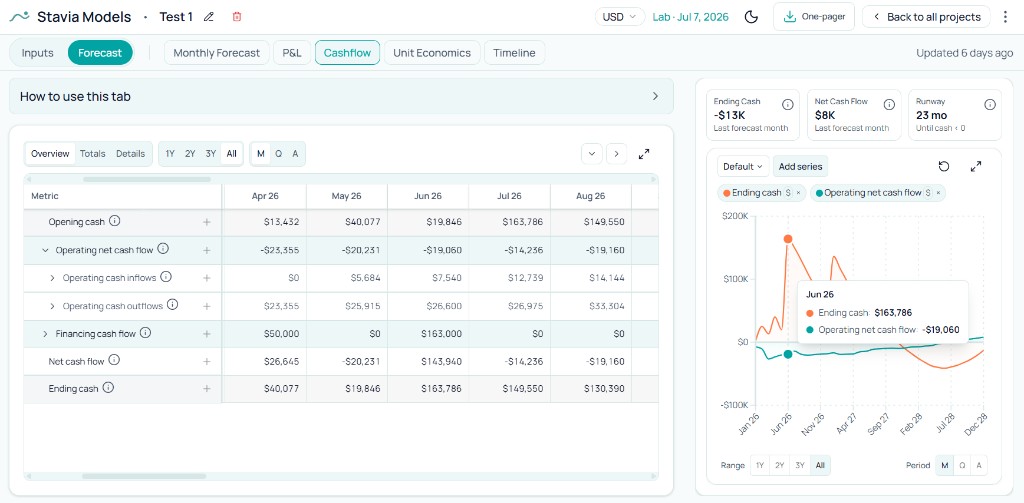

Cash Flow in a forecast is a rolling path, not a single headline. Ending cash at the horizon matters; the staircase that gets you there matters more. Runway should come from the month-by-month path of ending cash: when it first slips into the danger zone, whether financing clears that month, and whether operating net cash flow is bending toward sustainability. Average monthly burn is a rough shortcut; it will miss spikes, dips, and delays that a real plan contains.

A simple example keeps this concrete. Two modeled companies can show similar runway when you average burn, yet one still breaks first because a renewal slips by a month, a senior hire starts earlier than revenue catches up, or a round closes after ending cash has already crossed into negative territory. Cash Flow makes that sequence visible before it becomes a scramble.

The main layers of startup cash flow

In classic financial statements, cash flow is usually grouped into three sections: operating cash flow, investing cash flow, and financing cash flow. Operating cash flow is money collected and spent through the business itself. Investing cash flow usually covers purchases or sales of long-term assets, acquisitions, marketable securities, capital expenditures, or other investment activity. Financing cash flow is money from or returned to founders, investors, or lenders: equity raises, debt draws and repayments, dividends, buybacks, or similar financing movements.

For many early-stage SaaS, AI, and software startups, the most decision-relevant movements in a forecast are often the straightforward ones: customer collections, operating cash outflows, founder funding or venture rounds, then ending cash and runway. Investing cash flow can matter earlier for capital-intensive, infrastructure-heavy, hardware-heavy, or acquisition-driven companies. For a lot of young software teams, the first forecasting question is still concrete: do operations and planned financing leave enough cash to reach the next milestone?

Stavia's startup bridge below concentrates on that planning slice. Opening cash is the starting balance. Operating cash inflows are customer collections. Operating cash outflows are the cash costs of running and growing the business. Founder funding and investor rounds are the financing layer most teams model first. Ending cash is what remains in the bank and becomes the next period's opening balance.

Read it as a cash bridge: what the company started with, what operations did to it, what financing added, and what remains.

The startup cash bridge in Stavia

A planning shortcut for early-stage forecasts: not a full statement of every cash-flow line a public company files.

A common startup cash flow path

Most teams move through a recognizable sequence, even when the product and market differ. Use the path as a map, not a verdict: the same stage can look healthy or fragile depending on runway, milestone clarity, and whether cash is improving for operating reasons.

Negative operating cash in early stages is common. The serious questions are whether cash and time reach the next milestone, whether the operating trend improves for real reasons, and whether leadership is reinvesting on purpose or burning without progress.

Pre-revenue build

The company spends before it earns. Cash goes into product, tools, contractors, early team support, infrastructure, and launch preparation. Operating cash flow is usually negative, and the company depends on founder money, grants, consulting income, or early financing.

Early customer cash

Revenue starts, but it rarely covers the full cost base immediately. Monthly payments, annual prepayments, and first renewals begin to support the cash path, while payroll, acquisition, and product-serving costs can still be heavier than collections.

Growth investment

If the product starts working, the company often increases burn deliberately: more product development, more acquisition, more team, more infrastructure. Cash flow can get worse before it improves because the startup is investing ahead of scale.

Reinvest or harvest

Later, the company faces a strategic choice. A venture-backed startup often reinvests gross profit and operating cash into faster growth, keeping profit or free cash flow low because the goal is company value and scale. A different type of company may choose to preserve profit, build cash reserves, or pay dividends. Both paths are possible, but they imply different growth strategies.

Why revenue and cash are not the same

P&L revenue is recognized revenue under accounting rules. Cash Flow records when customers actually pay. Monthly billing tends to spread collections across the year; annual prepayment concentrates cash up front. That gap shapes runway and fundraising need: liquidity arrives earlier when customers prepay, even while revenue recognition smooths the income statement.

Two startups can show similar P&L revenue while carrying very different cash paths. The team with stronger annual collection and cleaner renewal timing may need less external cash for the same operating plan because customers finance more of the path up front. EBITDA sits on yet another line; it can improve while cash tightens when collections, cash-paid costs, or financing timing diverge from operating profit.

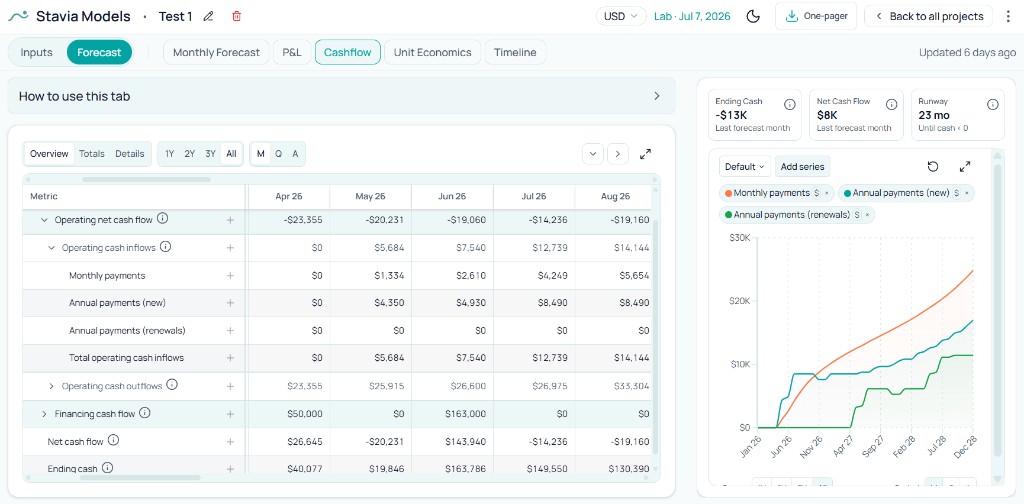

How operating inflows build cash

Operating inflows are not a copy-paste of revenue into a cash line. In Stavia they come from modeled payment behavior: monthly receipts, annual payments from new subscribers, and renewal cash each follow their own timing rules. That structure shows how pricing and billing choices move the bank balance, separate from how the P&L spreads recognition across periods.

Renewals matter more as the base matures: they can become repeatable cash support that reduces dependence on constant net new sales. A large annual collection month is welcome for liquidity; it still deserves a second look in operating net cash flow so you do not confuse one strong collection window with stable monthly engine health.

How operating outflows create pressure

Outflows are cash leaving for product-serving costs, acquisition, payroll, SG&A, tools, and one-time operating items. Usage-linked serving spend rises with volume — for AI products, see action-based AI product cost forecasting before free and trial tiers compress runway. Paid acquisition often leads payback. Payroll usually starts on a fixed calendar before the revenue impact of that hire fully appears. Overhead and subscriptions accumulate in ways that are easy to underestimate until you read them in cash. A legal project, brand sprint, or relocation can land in one month and carve a deep notch in ending cash.

Many cash problems are sequencing problems: the expense can be strategically sound and still early relative to incoming cash. That is why month-by-month Cash Flow stays closer to reality than a smoothed annual summary.

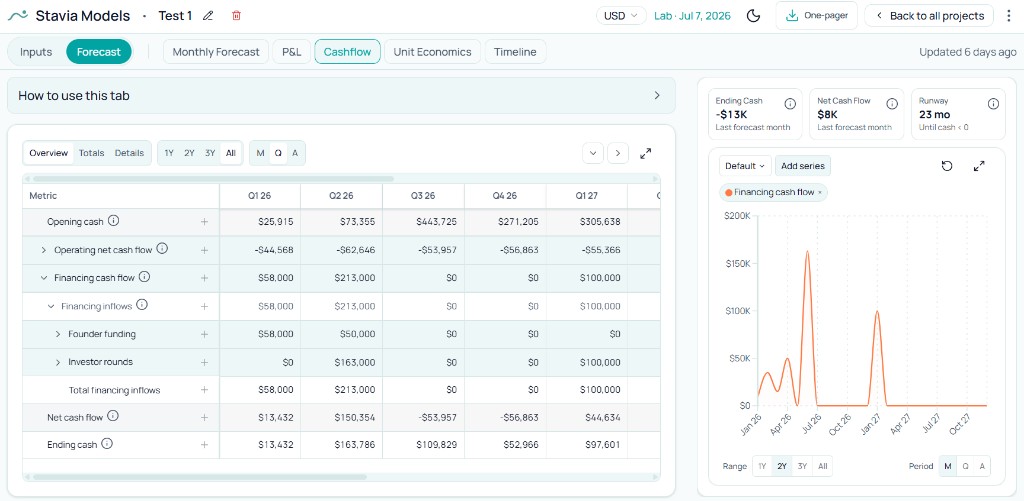

How financing changes the path

Financing shows up as cash entering the company: founder funding, investor rounds, or other modeled capital inflows. It extends runway on the cash path. It does not, by itself, repair EBITDA or prove that operating cash generation is healthy. An appropriately sized round can still land too late if the modeled closing month sits after the point where ending cash becomes dangerous. Founder capital can bridge an early stage without resolving long-term burn if operating net cash flow stays structurally negative.

Useful diligence questions include: which months this cash is meant to cover; which milestone it buys time to reach; whether it clears the window before ending cash turns negative; and what happens if the round slips, shrinks, or splits into tranches. Once financing timing is set, a startup use of funds plan connects the raise to spending blocks, milestone evidence, and monthly burn — not just a pie chart. Cash Flow turns those questions into a visible trajectory instead of a narrative slide.

How to read runway month by month

Average burn is a quick estimate; runway discipline lives in ending cash period by period. Identify the first month where ending cash crosses into uncomfortable territory, then check whether financing and operating recovery arrive before or after that point. Charts help separate whether the path improves because operating net cash flow is healing or primarily because financing lifted the balance.

If ending cash steps up right after a financing event while operating net cash flow stays deeply negative, the company has more calendar time; the operating path still needs work. That distinction keeps teams from confusing liquidity relief with operating recovery.

Public-company examples: why cash flow needs its own view

These examples are not benchmarks for an early-stage startup. Figma and Atlassian are mature software companies with scale, enterprise customers, stock-based compensation, and public-company reporting. They are useful because they show one simple lesson: a company's P&L result and cash flow result can look very different.

| Metric | Figma | Atlassian |

|---|---|---|

| Product | Design and collaboration platform | Collaboration and work-management software |

| Period | FY2025 | FY2025 |

| Revenue | $1.056B | $5.215B |

| P&L result | Large operating loss, heavily affected by IPO-related share-based compensation | Small operating loss |

| Operating cash flow | $250.7M positive | $1.460B positive |

| Free cash flow | $242.7MAdjusted free cash flow (as reported) | $1.416B |

| Simple lesson | A large accounting loss does not always mean the business consumed the same amount of cash. IPO-related share-based compensation moved the P&L heavily while operating cash flow stayed positive. | Customer collections can make cash flow much stronger than the P&L headline suggests. Read operating performance and cash movement as two separate views. |

Sources: Figma FY2025 official results / SEC filing · Atlassian FY2025 annual report · Atlassian FY2025 Form 10-K (SEC)

The lesson is not that early-stage founders should expect the same pattern. The lesson is that cash flow deserves its own view. P&L explains operating performance. Cash Flow explains money movement. When the two views disagree, ask what is driving the gap: customer collections, annual billing, deferred revenue, non-cash expenses, financing, or one-time events.

Why cash flow and P&L tell different stories

P&L and Cash Flow answer different questions, so they should be read together instead of collapsed into one headline. P&L focuses on whether the operating structure is improving: revenue, cost of revenue, gross profit, operating expenses, and EBITDA. Cash Flow focuses on liquidity timing: when customers pay, when payroll and vendors draw cash, when financing lands, and where ending cash sits each month in the forecast.

Annual billing can bring cash in earlier than revenue is recognized. Financing lifts ending cash without moving EBITDA. One-time costs can carve out a dangerous cash month even when the P&L slope looks smoother at a distance. Payroll and acquisition scale can pressure operating cash before the revenue line fully reflects the growth spend. Those gaps are normal in subscription businesses; the work is to see them in the forecast, not to be surprised by them in the bank account.

P&L helps founders judge whether the operating business is becoming healthier. Cash Flow should not be treated as a secondary report. It is the view that shows whether the company has enough time for the operating strategy to work.

How to use cash flow with the rest of the model

Start in Cash Flow when ending cash, runway, or operating net cash flow looks fragile. Cash Flow shows where the cash path breaks. Move next into the step-by-step forecast to locate the driver: billing, acquisition timing, serving cost, hire dates, one-time items, or financing assumptions. Open P&L to see whether operating structure is improving. Use Unit Economics in the product to test whether growth quality and payback support scaling the spend you are modeling. Return to financing inputs to stress whether funding timing covers the gap you see on the path.

How it works in Stavia Models

In Stavia Models, the Cash Flow tab is a planning view for early-stage startup forecasting. It does not try to reproduce every line of a full accounting cash flow statement. It focuses on the movements founders usually need first: customer collections, operating cash outflows, founder funding, investor rounds, net cash flow, ending cash, and runway. That keeps the view practical: you can see whether cash improves because operations are strengthening, because annual billing creates a collection spike, or because financing arrives. When the path turns fragile, move into the detailed forecast to find the driver.

You can read monthly, quarterly, or annual periods; for early-stage timing, monthly is usually the right lens. Overview, totals, and detailed modes move from the headline bridge into the rows behind a spike or dip. The chart panel can compare ending cash, net cash flow, operating inflows and outflows, financing series, and other selected lines so you can separate operating recovery from capital timing.

When pressure shows up, trace assumptions through acquisition, cost structure, overhead, and payroll; stress financing timing and milestones; and reconcile with P&L and Unit Economics so the story stays coherent across views.

Common mistakes when reading startup cash flow

Final thought

Cash Flow is where the forecast becomes operationally honest. It shows whether the strategy can be lived through in time. A founder can hold improving P&L, promising unit economics, and a credible growth narrative and still run into trouble when collection, spend, hire, and funding timing misalign.

The goal is larger than a single runway number. It is to understand what moves that number: collections, spending, hiring, acquisition, one-time costs, and financing timing, early enough that the company can adjust while options remain open. Cash timing is one view inside a financial model for startup decisions where P&L, unit economics, and financing share the same assumptions.

About the author

Anastasiia Nikolaeva

Founder of Stavia Models

Anastasiia Nikolaeva is a financial modeling consultant and the founder of Stavia Models. She has built financial models for SaaS, AI, marketplace, and other startup business models, helping founders plan pricing, growth, fundraising, and unit economics. Stavia Models is based on this hands-on consulting experience and turns that modeling logic into a guided product.