How to Model Cost Structure for an Early-Stage SaaS Startup

Separate product-serving costs, operating overhead, payroll, and one-time spend so your gross margin, burn, and fundraising plan reflect how the business actually works.

Stage your startup cost base

Test how product-serving costs, payroll, overhead, and one-time spend shape margin and burn from launch to the next stage.

24 months · launch vs scaling assumptions

Why cost structure matters

A startup cost model becomes weak when it treats every expense as part of one smooth monthly base.

That is rarely how an early-stage company actually works.

At the beginning, the business usually has a small core of costs that are truly necessary to launch and support the first stage. Around that core, there are other costs that may become important later: a broader team, more overhead, extra tools, more support, more process, more structure. Founders can often see those future needs quite clearly, and that is where the model starts to drift. The later-stage company enters the first-stage forecast too early.

Once that happens, the plan stops showing what the business needs now and starts showing a company that has already grown into a different stage. Burn rises too early. The fundraising ask gets heavier. The model becomes less useful for judging discipline.

The opposite problem exists too. Some forecasts stay too lean for too long and miss the cost structure that appears once traction starts to show up. Product-serving cost grows. Support becomes necessary. Hiring that looked optional becomes real. The company reaches the next stage, but the model still reflects the previous one.

That is why cost structure matters so much. It helps the founder build the company in stages on paper before trying to fund it in real life.

The four cost layers founders should separate

A useful cost model should separate costs by how they behave.

Some costs come from serving the product. Some are part of running the company. Some are tied to hiring and timing. Some belong to setup, launch, or a specific project. Acquisition spend matters too, but it deserves its own treatment because the logic is more connected to channel strategy, conversion, timing, and customer growth. That is why Stavia handles acquisition separately, and why this article focuses on the other main cost layers around it.

How startup costs behave in the model

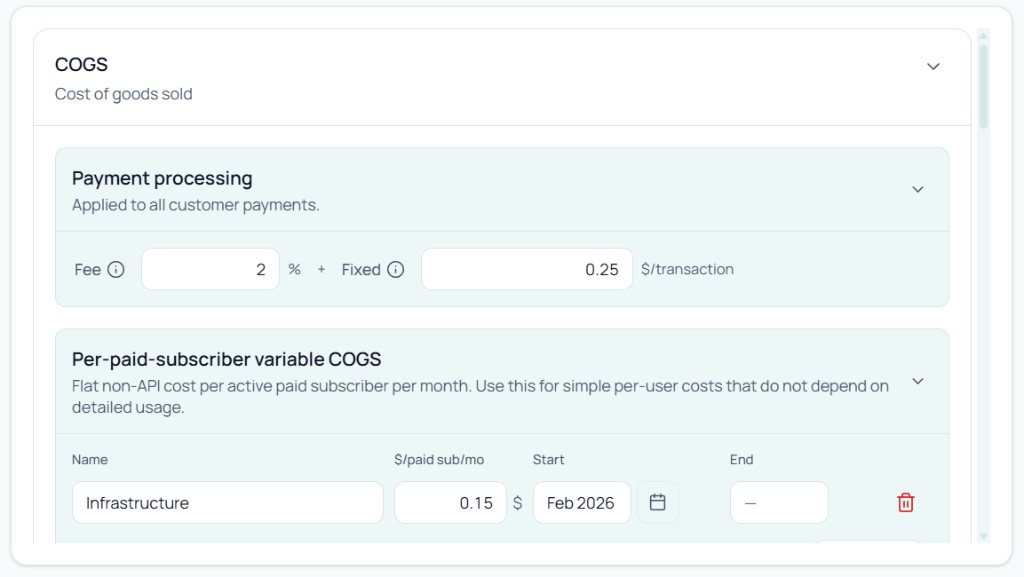

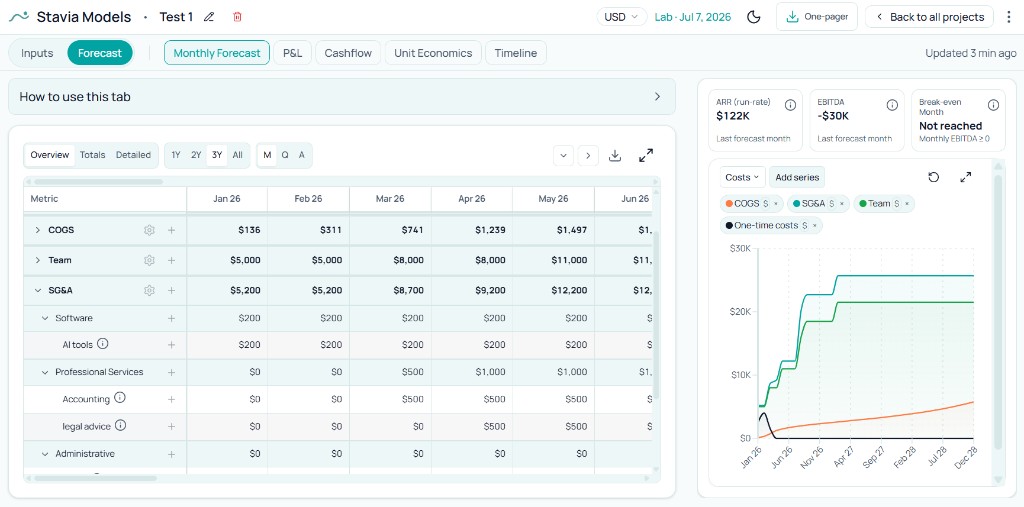

COGS

The cost of serving the product: payment processing, variable serving cost, usage-based APIs, AI features, and other costs that move with delivery of the product itself.

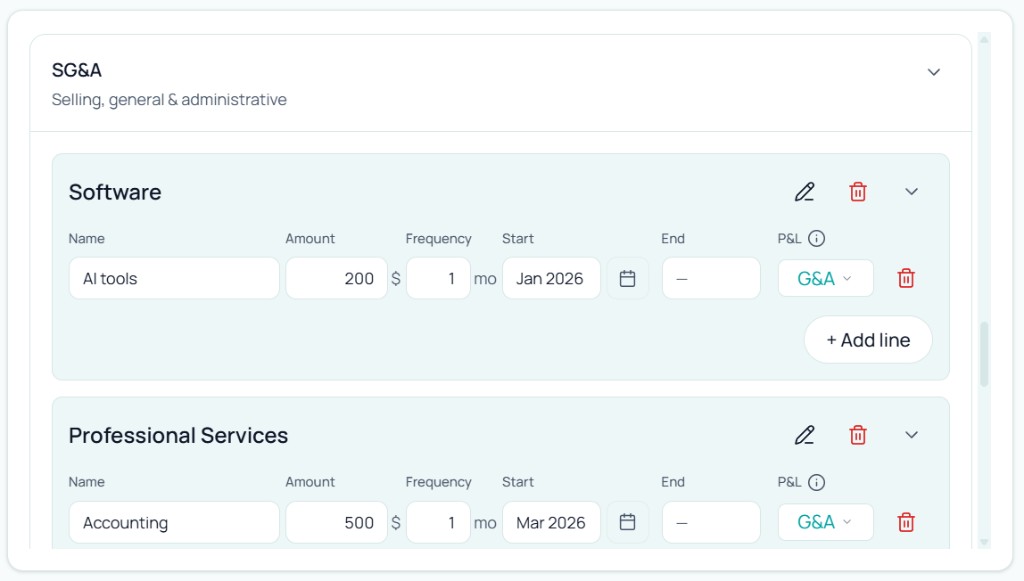

Operating expenses

Recurring non-payroll overhead: software, accounting, legal support, admin services, and the tools that help the company run.

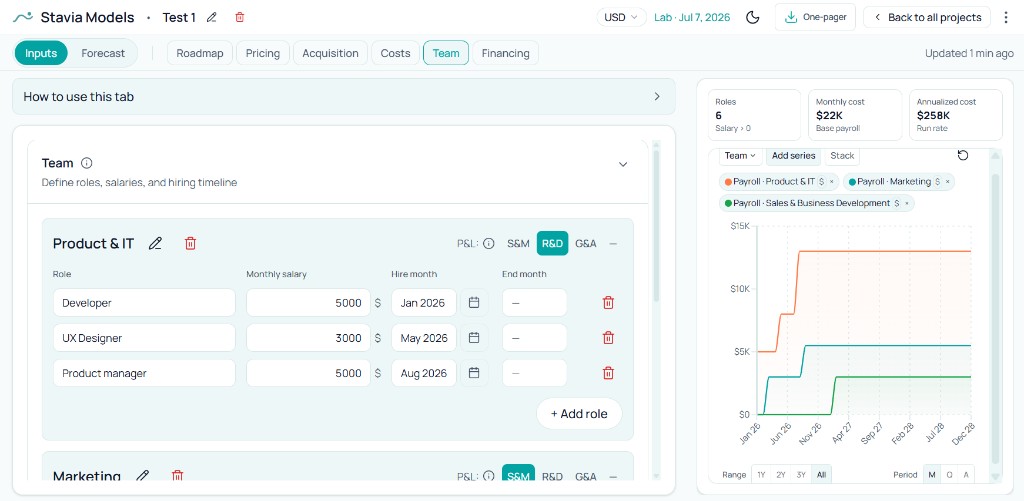

Payroll

Team cost with timing, roles, departments, and headcount decisions. This is usually the largest cost layer and should stay visible.

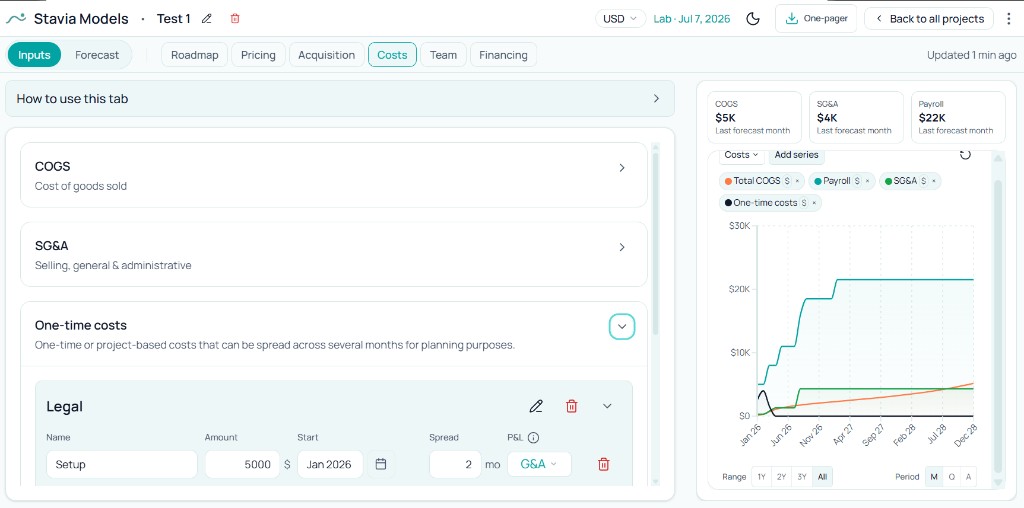

One-time costs

Setup, launch, legal work, branding, implementation, and other project-based spend that belongs to a phase, not to the permanent monthly base.

This structure is simple, but it already does a lot of work. It shows what affects margin directly, what builds the company around the product, what belongs to the next hiring step, and what should stay visible as temporary spend instead of disappearing into recurring overhead.

Timing matters more than founders expect

In consulting work, one of the most common modeling mistakes is putting too much of the future company into month one.

A founder already knows the team they would like to have, the tools they may need later, the support layer that will probably appear, and the overhead of a more mature business. Once those assumptions all enter the first stage of the forecast, the company starts looking heavier than it needs to be.

That creates a weak plan. The raise starts funding later-stage structure too early, and the model stops answering one of the most important early questions: what does this business actually need now?

The opposite mistake exists too. A model can stay too lean for too long and ignore the costs that appear once traction starts to show up. Product-serving cost grows. Support becomes real. Hiring that was optional in the first stage becomes necessary in the next one.

A good model does both jobs. It stays disciplined in the beginning and still leaves room for the cost structure that belongs to the next stage. Costs should follow milestones, product scope, and market progress. They should not all arrive in the first month just because the founder can already imagine them.

What belongs in COGS

COGS means cost of goods sold, or in startup language, the cost of revenue. This is the cost layer that answers a very direct question: what does it cost to deliver the product to a user and collect revenue from that user?

That is why COGS matters so much. It sits close to the product itself, and it shapes gross margin.

For an early-stage SaaS or AI startup, this category is often more complicated than founders expect. A few years ago, many products could model COGS quite lightly. Now the stack is often more variable. Payment processors take a share of transactions. Serving cost can depend on active subscribers. Third-party product APIs can scale with usage. AI features can create a new layer of cost that grows faster than expected if pricing and caps are too generous. When COGS boundaries are unclear, which costs belong in cost of revenue is a useful reference. When AI or API usage is material, forecast AI/API costs before launch belongs in the same layer.

That is why it helps to think about COGS as the part of the model where product delivery becomes economic reality. If the founder wants to understand whether pricing is strong enough, whether an AI feature is too expensive, whether free usage is too generous, or whether usage-based vendor cost is starting to weaken margin, this is the layer where those questions become visible.

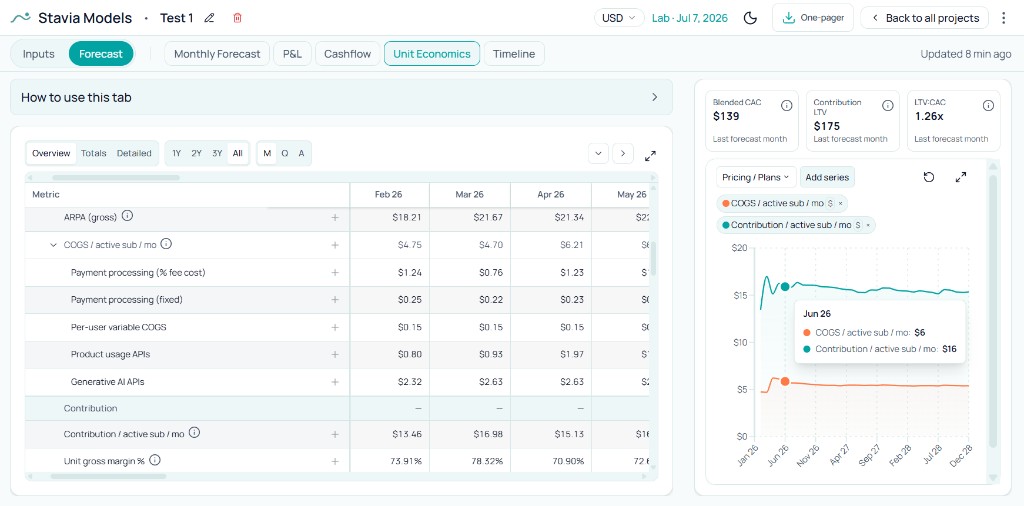

A good COGS structure should also reflect that these costs do not move in the same way. Payment processing follows transactions. Per-user serving cost follows active users. Product usage APIs and AI APIs follow the specific behavior of the feature. Trial or free serving cost can exist before the paid base is large enough to support it. That is exactly why a single average cost assumption usually becomes too weak.

What belongs in operating expenses

Operating expenses are the costs of running the company around the product.

This is where a lot of the practical overhead of an early-stage startup sits: software subscriptions, accounting, legal support, admin services, and similar recurring costs that matter for burn even though they are not directly tied to serving one more active user.

This section needs a little care because "operating expenses" in a broad finance sense can include payroll and acquisition spend too. Here, the useful distinction is narrower. In this article, we are talking about recurring non-payroll overhead. Payroll deserves its own section because hiring has timing and headcount logic. Acquisition deserves its own article because channel spend depends on different assumptions altogether.

What matters for founders is not only what goes into overhead, but when it starts. An AI tool subscription may belong from the first month. Accounting support may begin later. Legal support may become recurring only once the company structure or commercial activity becomes more complex. When staging overhead, a separate startup overhead budget helps keep recurring setup costs honest by milestone. The model becomes much more useful when those costs arrive at the stage they actually belong to, instead of sitting in the forecast from the very beginning without any real timing logic.

This is also where the modern early-stage reality matters. AI tools can substitute for some manual work, especially in the first stage of the company. A founder may need fewer people to reach MVP than would have been realistic a few years ago. Some work that would previously have required another hire can now be supported by AI subscriptions or agents. In the model, those costs often belong in overhead rather than payroll. That does not remove the need for strong people. It changes how the first stage of the team and cost base can be built.

How to plan payroll in an early-stage model

Payroll is still one of the biggest cost layers in most IT and SaaS startups, even if the first stage can now be leaner than it used to be.

The key question is not whether payroll is "special" in theory. The key question is how to model it in a way that matches real hiring decisions.

A useful payroll plan is built around departments, roles, hire timing, and headcount logic. Product and engineering hiring usually follows product scope and launch milestones. Marketing hiring often depends on whether acquisition has started to work. Business development and administrative roles usually belong to later stages than the first version of the product. That timing matters much more than one growing salary line.

This is also where the current startup environment has changed. Founders can now sometimes build the first stage of a product with a smaller team than they would have needed before, especially if they can use AI tools or coding agents well. That does not mean people are no longer important. It means the first version of the company can sometimes reach MVP or early traction with fewer hires, and the model should reflect that possibility honestly.

Then, once the company begins to grow, payroll becomes the place where the next stage shows up very clearly. More product work, more support, more sales motion, more internal structure — that is where the team plan should expand. Headcount and payroll timing is where hiring choices turn into monthly burn. The useful model is the one that shows both stages: the disciplined first version and the larger operating shape that may come later.

Why one-time costs need their own place

One-time costs are easy to underestimate because they are temporary. They still matter a lot.

Legal setup, branding work, implementation help, launch support, special product work, or market-entry projects can create real pressure on cash even if they do not belong in the steady monthly run rate.

That is why one-time costs should have their own place in the model. They show which spend belongs to a phase, a launch window, a setup period, or a special project. Without that visibility, temporary work either disappears into the model or distorts the permanent cost base.

In Stavia, one-time costs are modeled as project-based amounts with a start month and a spread period. That is practical for planning because it reflects the shape of setup work without treating it as if it were normal monthly overhead.

This distinction becomes especially useful when the founder is preparing a fundraising story. Investors should be able to see which costs are structural and which costs belong to the current stage.

That visibility matters because one-time costs often sit close to the moments when a startup is most financially fragile: launch, legal setup, rebrand, fundraising prep, implementation work, or entry into a new market. They are temporary, but they can still shape runway in a very real way. A good model should make that visible instead of flattening everything into the monthly base.

How this changes gross margin, burn, and fundraising

Cost structure matters because each of these layers changes a different part of the company's financial story.

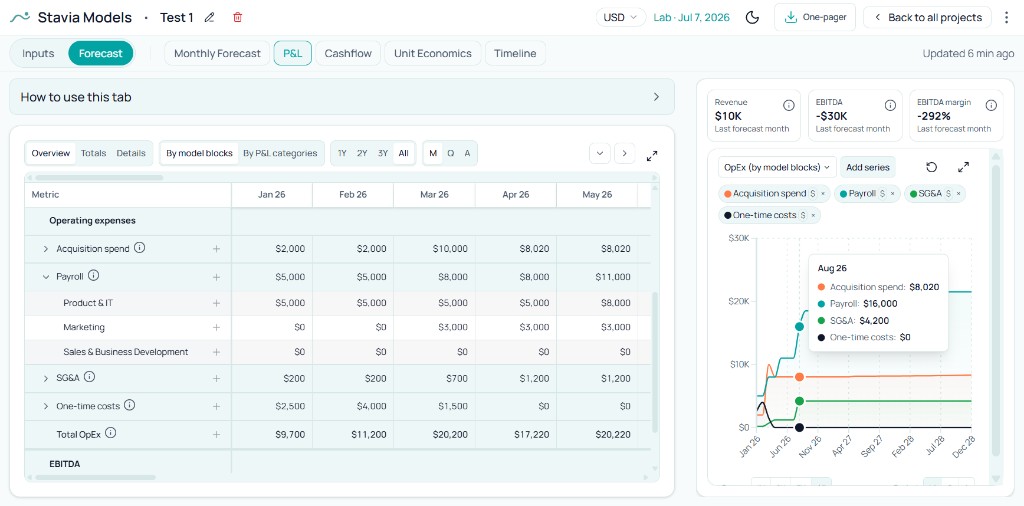

COGS changes gross margin. It shows how much room is left after the product is delivered. If product-serving cost rises too fast, pricing starts to look weaker. If COGS is too simplified, gross margin can look healthier than it really is.

Operating expenses, payroll, one-time costs, and acquisition spend shape operating burn below gross profit. They tell the story of what it takes to build and run the company around the product. This is where the business starts to show whether it is scaling with discipline or simply becoming heavier.

That distinction matters because founders need more than one financial lens. They need to understand whether the product works economically, and they need to understand how much cash the company needs to support the current stage and the next one. Those are different questions, and the model should be able to answer both.

This is where the Monthly Forecast becomes useful. It shows when different cost layers step up, how early burn starts to expand, and which assumptions are responsible for that change. A founder can see whether the pressure is coming from product-serving cost, from hiring, from overhead, or from a temporary project.

The P&L view adds another perspective. At a high level, investors and operators often want to see costs through familiar P&L categories such as Sales and Marketing, Research and Development, and General and Administrative. That is useful because it connects the detailed model to the language used in investor reporting and public-company financial statements. In Stavia, the product can also show P&L through those categories, which helps the founder move from modeling detail to a cleaner, more standard financial presentation.

That is also where benchmarking becomes more practical. Early-stage benchmarking is rarely perfect, but founders can still learn a lot from public companies. A SaaS founder can look at investor pages and filings from companies with a similar business model or vertical and study the broad structure: what share of revenue goes into COGS, how operating expenses are grouped, and how R&D, Sales and Marketing, and G&A are presented at a high level. Figma's investor relations pages are a good example of that kind of public reference point.

Then there is unit economics, which answers a narrower question. Unit economics focuses on the economics of serving and monetizing paying users. Company-level gross margin can include other serving cost too, including the cost of trial or free users. That is why unit margin and company margin are related, but they are not the same thing. For founders, that difference is useful. It separates the question "does this paid user work?" from the question "does the whole company margin work at this stage?"

This is also why cost structure matters so much in fundraising. A founder who can explain the difference between product-serving economics, operating buildout, and temporary project spend is in a much stronger position than a founder who can only show one blended burn number.

Common mistakes

These are planning mistakes, not bookkeeping mistakes. Catching them early makes the whole model more useful.

How to organize this in Stavia

A good workflow in Stavia starts with cost layers, not with a long undifferentiated list.

Build COGS around the real cost of serving the product. Add recurring non-payroll overhead under SG&A. Add one-time costs for setup, launch, legal, branding, implementation, or project work. Keep payroll in Team, where timing and department logic belong.

Then read those costs back through the model.

Use Monthly Forecast to see how cost layers build over time.

Use P&L to understand what affects gross profit and what sits below it.

Use Unit Economics to see how paid-serving cost shapes contribution and margin.

That is where the product becomes useful as a planning tool. It stops being a place to enter rows and becomes a way to test whether pricing, cost discipline, hiring pace, and fundraising logic fit together.

Conclusion

A clean cost structure makes an early-stage model more honest.

It shows what the product costs to serve. It shows what the company costs to run. It shows which spend belongs to the first stage, which spend belongs later, and which costs are temporary even when they are very real.

That matters before fundraising because investors are backing more than the idea. They are backing the founder's ability to build with discipline, stage by stage, and to ask for capital that matches the real shape of the next milestone. Those layers connect inside a connected startup financial model where pricing, acquisition, and runway share one forecast.

About the author

Anastasiia Nikolaeva

Founder of Stavia Models

Anastasiia Nikolaeva is a financial modeling consultant and the founder of Stavia Models. She has built financial models for SaaS, AI, marketplace, and other startup business models, helping founders plan pricing, growth, fundraising, and unit economics. Stavia Models is based on this hands-on consulting experience and turns that modeling logic into a guided product.